The past month will undoubtedly go down in history, although it ultimately ends with a near-stalemate in the stock indices. The S&P 500 finishes barely in the red (-1%), as does the Stoxx 600 (-2%), with one major caveat: the dollar has significantly worsened its decline in April (-4%), further adding to an already painful note since the beginning of 2025, with a cumulative drop nearing 9%.

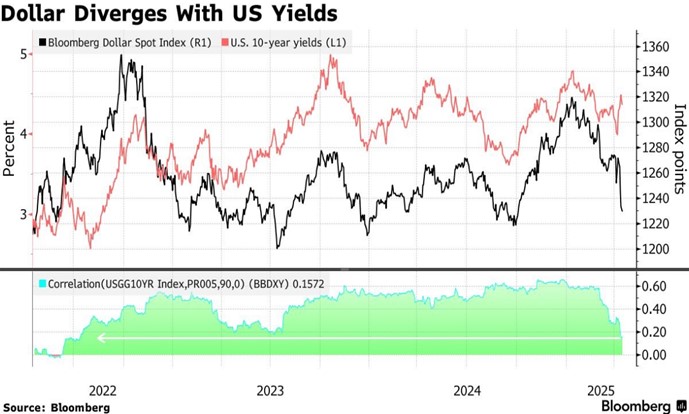

It was, in fact, the bond market shocks at the start of the month — with the 10-year yield rising from 3.9% to 4.5% in just five sessions — combined with the weakness of the dollar, that brought Donald Trump back to a bit more reason on April 9, after the absurd "Liberation Day" scenario. Not only were interest rates rising uncontrollably, but — an extremely rare phenomenon — the dollar itself was depreciating rather than strengthening. In other words, investors were beginning to retreat from the dollar zone.

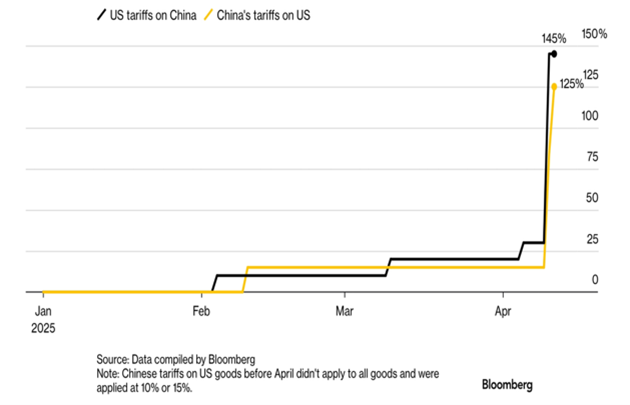

Decline in the correlation between long-term rates and the dollar – Evolution of tariffs since 2025.

The current situation regarding tariffs is obviously neither desirable nor sustainable, as it risks bringing international trade to a halt, resulting in only losers. The consensus is therefore to logically anticipate a softening of the U.S. position, as production chains cannot adapt in just 90 days. We are already seeing early signs of this, notably with the reduction of tariffs in the automotive sector. However, it seems optimistic to expect a quick return to normal, especially with China. Neither the Trump administration nor the Chinese government are solely pursuing economic rationality. If that were the case, U.S. tariffs on Chinese imports would not be set at 145%, and those imposed by China on U.S. products would not be at 125%. The negotiations, on the contrary, could last a long time.

Indeed, Chinese authorities may prioritize national dignity and sovereignty over corporate profits, even if it results in a modest slowdown of economic growth. After all, exports to the U.S. account for only 2.6% of China's GDP. Standing up to "American imperialism" would bring much more political gain to the Chinese Communist Party than quickly yielding to American demands. Conversely, the United States may soon realize just how dependent it is on high-value Chinese imports. Time should therefore work against them, with an increased risk of shortages, which could force Trump’s hand — even leading to a possible capitulation — if his popularity drops significantly. Xi Jinping, for his part, will not be constrained by such considerations.

At present, we do not have precise information on the state of the U.S. economy since April 2. Even the earnings season (which was relatively good, but ends on March 31) offers no clear indications. Its resilience actually contributes to increasing the confusion, as opinion polls — sometimes unreliable — suggest a significant contraction in economic activity in the coming weeks. How to explain this discrepancy? It is due to logistical delays: it takes between 20 and 40 days for Chinese containers to reach the U.S. The sharp drop (from 30% to 50%) in the number of containers en route since mid-April will not be felt in U.S. ports until mid-May, and goods shortages will not appear until mid-June. The shock is therefore ongoing, but it is still too early to fully feel its effects. Only a quick agreement could mitigate the impact; otherwise, a recession seems inevitable. As always, investors hope the Fed will intervene, but it is constrained by the expected rise in inflation due to tariffs. Similarly, the still-high budget deficit (6%) prevents any short-term economic stimulus.

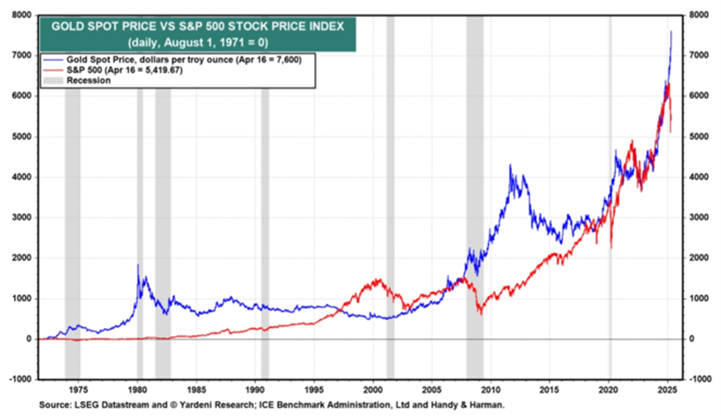

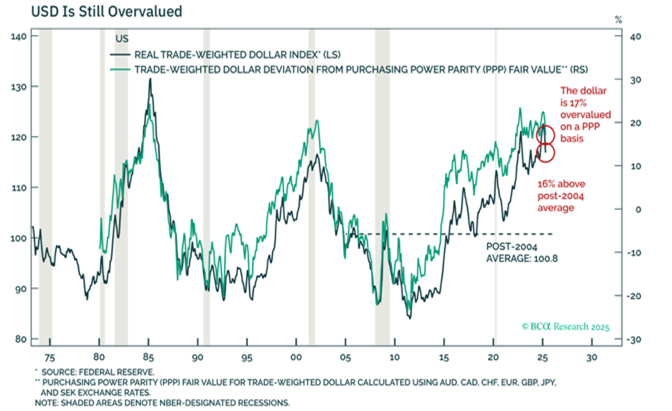

The situation is therefore both uncertain — as it can be resolved at any moment — and complex, due to the many geopolitical factors at play. Even in the case of an agreement, a full return to the previous situation seems unlikely. Certainly, any good news on this front would support U.S. markets, but it has now become clear that an agreement with the United States is only valid as long as it serves their interests. Moreover, the devaluation of the dollar is a barely concealed objective. Thanks to continuous money printing, U.S. growth has become excessively dependent on rising asset prices (real estate or financial), which has overly supported American household consumption, financed by global savings. The outperformance of gold compared to the S&P 500 since the abandonment of the dollar's convertibility in 1971 clearly illustrates this dynamic.

Evolution of gold price (in blue) and S&P 500 (in red) since 1971 — The dollar is currently overvalued by approximately 20% relative to its purchasing power parity (PPP).

In this context, is it still justified to hold so many dollar-denominated assets? The share of the U.S. stock market in the global index is nearly 65%, while U.S. corporate profits represent only 43% of the total, and the U.S. GDP only 27%. Shouldn’t we consider reducing this overexposure, especially given such an unpredictable administration? This is likely the analysis currently being made by foreign investors, which should encourage a redirection of flows toward the European market. For reference, European investors hold about 20% of all U.S. stocks, equivalent to nearly three-quarters of the total market capitalization of the Stoxx 600.

We therefore reiterate our recommendation made at the beginning of the year: against the consensus, we continue to believe that caution should prevail over euphoria, and the U.S. market should be underweighted relative to its benchmark. In terms of investment style, it is essential to maintain balanced diversification, without focusing exclusively on large U.S. growth stocks. The unpredictability of Donald Trump will continue to fuel volatility. And since all surveys show that private and institutional investors remain heavily overweight in U.S. equities compared to historical averages, it is likely that the trend reversal has only just begun.